AI financial risk is defined as the range of financial stability, institutional, and conduct risks that arise when artificial intelligence technologies are used in financial decision-making, operations, and markets. The Financial Stability Board (FSB) frames this as an enterprise-wide governance challenge, not a narrow IT problem. Understanding AI financial risk means recognizing that AI changes not just how decisions are made, but how failures cascade across interconnected systems. Credit scoring, fraud detection, algorithmic trading, and loan underwriting all now carry AI-specific risk profiles that traditional risk frameworks were not built to handle.

What is AI financial risk and why does it matter now?

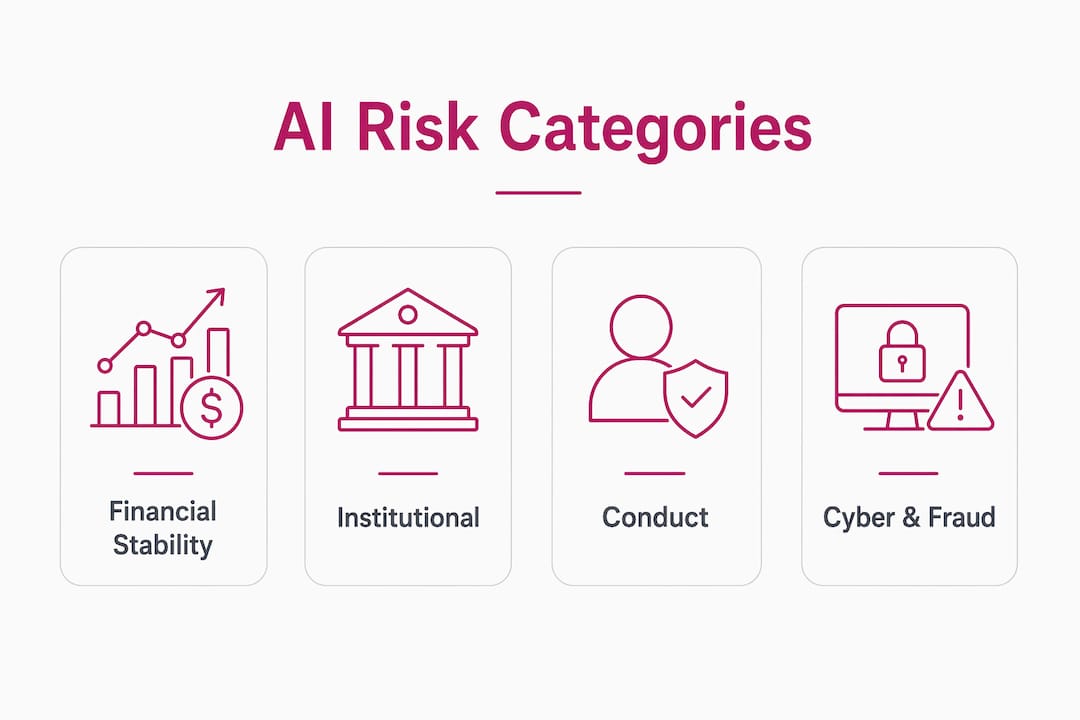

AI financial risk encompasses three distinct layers: financial stability risk, institutional risk, and conduct risk. Financial stability risk refers to the potential for AI-driven behaviors to amplify market shocks or trigger systemic failures. Institutional risk covers the operational, model, and data failures that affect individual firms. Conduct risk addresses how AI influences customer outcomes, including biased credit decisions or manipulative pricing.

The FSB’s 12 sound practices framework, published in 2026, groups these risks across governance, lifecycle risk management, and cyber and ICT risk categories. That structure reflects a core insight: AI risk is not a single event but a continuous exposure that evolves as models are trained, deployed, and updated. Executives who treat AI risk as a one-time model validation exercise will miss the majority of their actual exposure.

The impact of AI on finance is already visible in credit underwriting at firms like JPMorgan Chase, fraud detection at Visa, and trading operations at Renaissance Technologies. Each use case introduces a distinct risk profile that demands specific controls.

What are the main categories of AI financial risk?

AI financial risk breaks into four primary categories, each with distinct sources and failure modes.

Governance risk arises when accountability for AI decisions is unclear. When a credit model denies a loan, who owns that decision? If no human can explain or override the output, the firm faces both regulatory and reputational exposure.

Lifecycle risk covers every stage from data collection through model deployment and retirement. A model trained on pre-pandemic consumer behavior, for example, will produce systematically wrong credit risk assessments when economic conditions shift. The FSB lifecycle approach requires firms to map AI outputs to their material impact and permissions at each stage.

Cyber and ICT risk is amplified when AI systems become critical infrastructure. A compromised AI model in a trading system can execute thousands of harmful transactions before any human notices.

Third-party risk is the most underestimated category. Most financial institutions do not build their own AI. They buy it from vendors like Microsoft, Google, or specialized fintech providers. That dependency creates concentration risk when multiple firms rely on the same underlying model or cloud infrastructure.

- Model risk: AI models can fail silently, producing confident but wrong outputs

- Data risk: Biased or incomplete training data produces biased decisions at scale

- Operational risk: AI systems can act faster than human oversight can respond

- Emerging threats: Agentic AI systems that take autonomous actions introduce entirely new failure modes

Pro Tip: Map every AI use case in your organization to one of these four categories before you build any governance program. A use-case inventory is the foundation of effective financial risk assessment with AI.

How do AI architectures affect financial stability?

The design of an AI system, not just its accuracy, determines its systemic risk profile. This is one of the most underappreciated findings in recent financial stability research.

The European Central Bank published research in 2026 comparing two AI architectures used in financial simulations. The results were striking.

| Architecture | Behavior under stress | Systemic risk profile |

|---|---|---|

| Q-learning (reinforcement learning) | Highly coordinated, simultaneous actions | Extreme, bank-run-like dynamics |

| Large language models (LLMs) | Less coordinated, more unpredictable | Diffuse but harder to anticipate |

ECB simulations show that Q-learning agents, when deployed across multiple institutions, can produce coordinated behaviors that resemble bank runs, even without any explicit communication between systems. That coordination is an emergent property of shared training environments and similar reward functions. LLMs produce less coordinated but more unpredictable outcomes, which creates a different kind of systemic fragility.

The practical implication is significant. An AI system that performs well in isolation can become dangerous when many institutions deploy similar architectures simultaneously. Standard accuracy metrics do not capture this risk. The ECB recommends stress-testing AI systems in multi-agent scenarios to surface coordination-driven fragilities that single-model evaluations miss entirely.

Financial instability, in this context, is an emergent property of the AI decision ecosystem, not a failure of any single model.

Pro Tip: When evaluating AI vendors for trading or portfolio management, ask specifically how their architecture behaves under correlated stress scenarios. A vendor who cannot answer that question has not done the work.

What cyber and fraud risks does AI introduce to finance?

AI does not just create new risks. It dramatically amplifies existing ones.

The International Monetary Fund has identified AI-fueled cyber threats as a core financial stability concern. Advanced AI tools reduce the time and cost required to discover and exploit system vulnerabilities. That means attackers can now probe financial infrastructure at machine speed, identify weaknesses, and launch coordinated attacks before defenders can respond. The IMF warns that this raises the likelihood of correlated failures across multiple institutions simultaneously, which is the definition of a systemic shock.

Generative AI has changed the fraud equation just as dramatically. Fraud schemes that once required skilled human operators can now be executed at scale by automated systems. Deepfake audio and video make social engineering attacks far more credible. Phishing emails generated by large language models are grammatically perfect and contextually convincing in ways that traditional filters were not designed to detect.

RSM’s financial services practice outlines a practical control framework for AI-enabled fraud:

- Shift detection earlier in the fraud funnel. Transaction monitoring at the point of payment is too late. Behavioral analytics that flag anomalies in login patterns, device usage, and session behavior catch fraud before money moves.

- Enforce dual approval for high-value transactions. A single authorized user should never be sufficient to initiate a large wire transfer. Dual approval controls remove the single point of failure that AI-enhanced social engineering exploits.

- Implement call-back checkpoints for payment instruction changes. When a vendor or counterparty requests a change to payment details, a verified phone call to a known number is a high-friction control that AI-generated fraud cannot easily bypass.

- Build systems-level controls, not just policy controls. Policies that require human review are only as strong as the humans following them. Embedding controls directly into payment systems removes reliance on manual compliance.

The core insight from RSM is that AI-generated fraud schemes exploit social engineering better than any previous attack vector. The defense must be structural, not behavioral.

What governance frameworks guide responsible AI adoption in finance?

The FSB’s 12 sound practices, organized across three categories, provide the most comprehensive public framework for AI risk management in financial institutions.

Governance practices cover board-level accountability, AI risk appetite statements, and clear ownership of AI decisions. The FSB expects institutions to treat AI governance as a board-level responsibility, not a technology department function.

Lifecycle risk management practices address how institutions manage AI from initial design through deployment and decommissioning. This includes model validation, data quality controls, performance monitoring, and change management protocols. A Springer review of AI risk management in finance emphasizes the shift toward managing decision architecture and human oversight, not just model accuracy metrics.

Cyber and ICT risk practices focus on the resilience of AI infrastructure, third-party dependencies, and incident response capabilities specific to AI system failures.

The Federal Reserve’s position adds an important nuance. The Fed’s amended model risk management guidance excludes generative and agentic AI from its traditional model risk management scope. That exclusion does not mean these tools are ungoverned. The Fed expects firms to maintain a comprehensive inventory of all AI tools, apply tiering and independent challenge processes, and govern these systems through risk, compliance, and audit functions. Generative and agentic AI must be treated as governed assets under broader safety and soundness frameworks.

Executives building an AI governance program should prioritize three practical steps:

- Build a complete AI use-case inventory, tiered by material impact and permissions

- Integrate human-AI decision workflows so that consequential decisions always have a human checkpoint

- Conduct multi-agent stress tests annually to surface emergent systemic risks

The AI governance trends shaping 2026 regulatory expectations all point in the same direction: governance must be proactive, documented, and continuously monitored.

Key Takeaways

Effective AI financial risk management requires enterprise-wide governance, architecture-aware stress testing, and structural fraud controls, not just model validation.

| Point | Details |

|---|---|

| Define risk by category | Map AI exposure across governance, lifecycle, cyber, and third-party risk before building controls. |

| Architecture determines systemic risk | Q-learning systems can produce bank-run dynamics; stress test AI in multi-agent scenarios, not isolation. |

| Fraud controls must be structural | Dual approval and call-back checkpoints embedded in systems outperform policy-based controls against AI fraud. |

| Generative AI needs governance | The Fed excludes it from model risk management but requires inventory, tiering, and independent challenge. |

| Lifecycle risk is continuous | AI risk does not end at deployment; performance monitoring and change management are ongoing obligations. |

The governance gap executives keep ignoring

The most common mistake I see financial executives make is treating AI risk as a model risk problem. They assign it to the model validation team, run the standard accuracy tests, and consider the job done. That approach misses the majority of actual exposure.

AI financial risk is fundamentally a governance and decision architecture problem. The question is not whether a model is accurate in testing. The question is what happens when that model is wrong at scale, when multiple institutions are running similar models simultaneously, and when no human in the loop has the context or authority to override the output quickly enough to prevent harm.

The ECB’s finding on emergent coordination effects should change how every executive thinks about AI procurement. When your institution and your competitors all buy AI from the same small pool of vendors, you are not just adopting a tool. You are joining a shared behavioral ecosystem. The systemic risk that emerges from that ecosystem is invisible at the individual firm level and only visible when you stress test the whole system together.

The executives who will manage AI financial risk well are the ones who treat it as an enterprise governance issue from day one. They build inventories before they build controls. They ask vendors hard questions about architecture and stress testing. They integrate human checkpoints into AI decision workflows before regulators require them to. Proactive governance is not a compliance cost. It is the only way to capture AI’s benefits without inheriting its systemic risks.

— TekkrTools

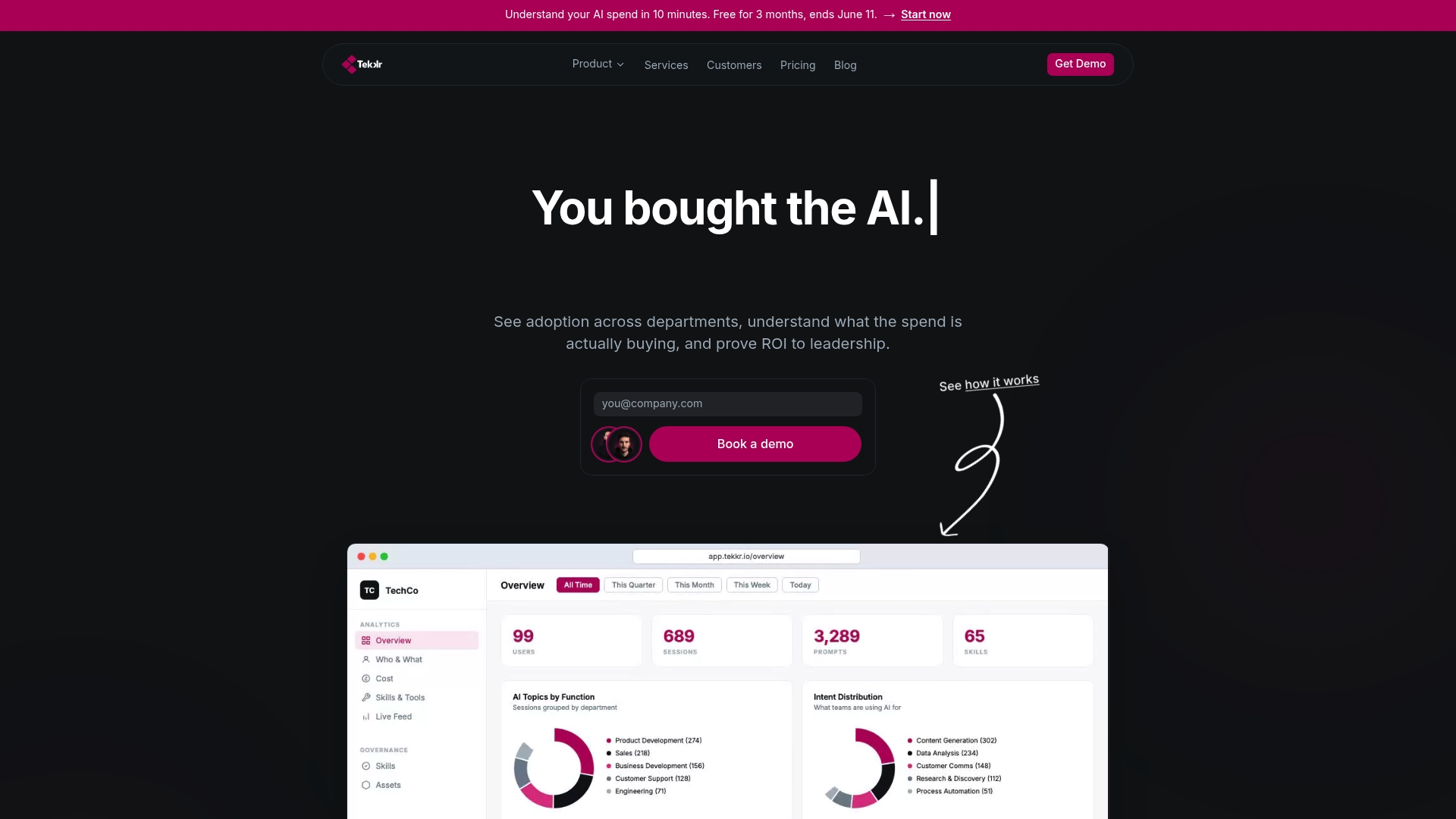

How Tekkr helps financial institutions manage AI adoption risk

Financial institutions deploying AI face a specific challenge: they need visibility into what AI tools are actually being used, how they are being used, and whether the adoption is generating measurable returns or creating unmanaged exposure.

Tekkr’s AI adoption platform gives executives exactly that visibility. Configurato tracks AI tool usage across every team, breaks down costs by department, and surfaces use-case intelligence that shows where AI is working and where it is creating risk. For financial institutions navigating FSB and Federal Reserve governance expectations, that kind of documented oversight is not optional. Tekkr’s privacy-first architecture is end-to-end encrypted, GDPR-compliant, and strips PII automatically, so adoption tracking does not create new data risk. Setup takes about 10 minutes, with a free tier and no credit card required.

FAQ

What is AI financial risk in simple terms?

AI financial risk is the set of risks that arise when AI systems are used in financial decisions, including the risk of model errors, systemic market instability, cyber vulnerabilities, and conduct failures that harm customers or markets.

How does the FSB define AI financial risk?

The FSB defines AI financial risk across three categories: financial stability risk, institutional risk, and conduct risk. Its 12 sound practices framework provides structured guidance for managing these risks across governance, lifecycle, and cyber dimensions.

Why do AI architectures matter for financial stability?

Different AI architectures produce different systemic behaviors under stress. ECB research shows Q-learning systems can trigger coordinated bank-run dynamics across institutions, while LLMs produce less coordinated but more unpredictable outcomes.

Does the Federal Reserve regulate generative AI under model risk management?

The Fed’s amended model risk management guidance excludes generative and agentic AI from its traditional scope. However, the Fed still expects firms to govern these tools through risk, compliance, and audit frameworks, including maintaining a full inventory and applying independent challenge processes.

What is the single most effective control against AI-enabled fraud?

Structural controls embedded directly in payment systems, specifically dual approval requirements and call-back checkpoints for payment instruction changes, are the most effective defense against AI-enhanced fraud schemes that exploit social engineering.